Do Autographs Increase in Value

Determining whether historical autographs increase in value: A study

Since we started in this field in the 1980s, we have often been asked whether autographs make good investments. It is a fair question, and over the years we came to feel that the answer, which was “sometimes”, raised more questions than it answered. Despite its importance, there had never been an independent study on the subject, and lacking that we were constrained in our response. The only information we found out there was frankly disinformation, misleading numbers and unsupported claims pumped up by people with questionable ethics who were selling autographs flat out as great investments.

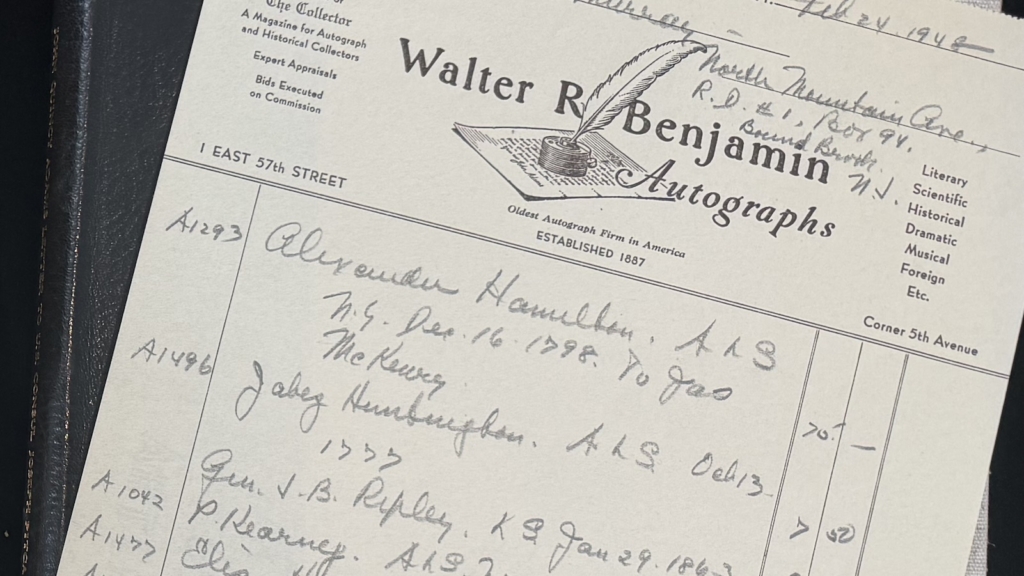

About a decade ago The Raab Collection determined to seek out an objective answer, one that would be provided by a disinterested third party with unquestionable knowledge and experience in the field of Applied Statistics and Probability Models. We approached the Wharton School of Business at the University of Pennsylvania, and Professor Abraham J. Wyner agreed to perform the study. To provide Dr. Wyner with the statistics, over the course of months we delved into autograph catalogs going back to 1887, hundreds of them, many yellowed and fragile, poured out across our conference table. We used the catalogs of the best dealers of the era, most being issued by Walter R. Benjamin and Thomas Madigan, as well as auction results in Book Prices Current and others found in now-obscure reference books. We concentrated on intervals we knew were watersheds, and avoided anomalies, starting in 1892 when Benjamin had been in business five years and the concept of autograph dealing had taken root, then went to 1922 after the slump of World War I had ended and fields like autographs and art received notice, then went to 1949 to avoid the World War II years and catch the post-war era early on, then on to 1962 in the Kennedy years, then up to 1992 when the increase in prices had manifested, and 2002 which was the last year for which detailed statistics were then available.

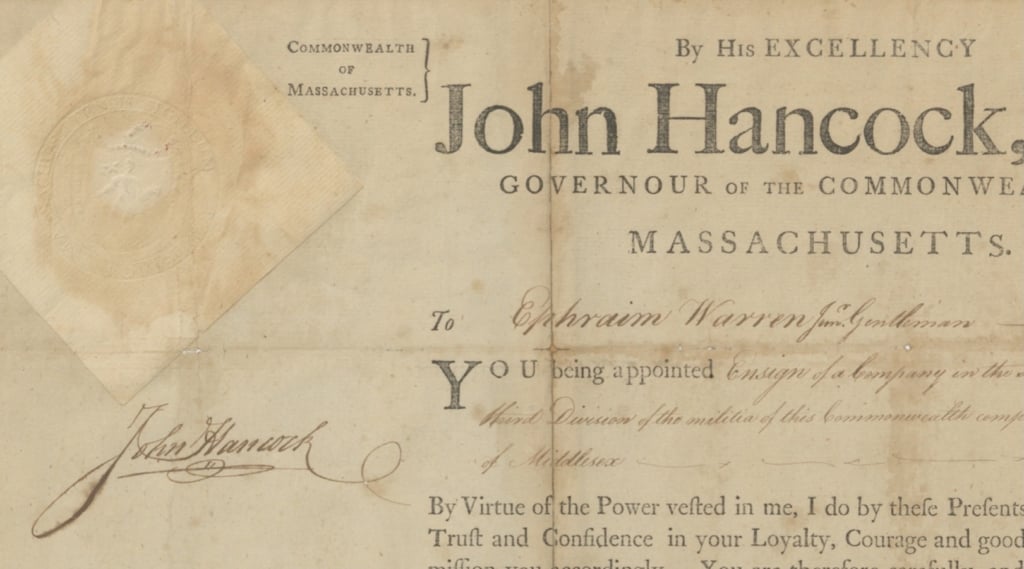

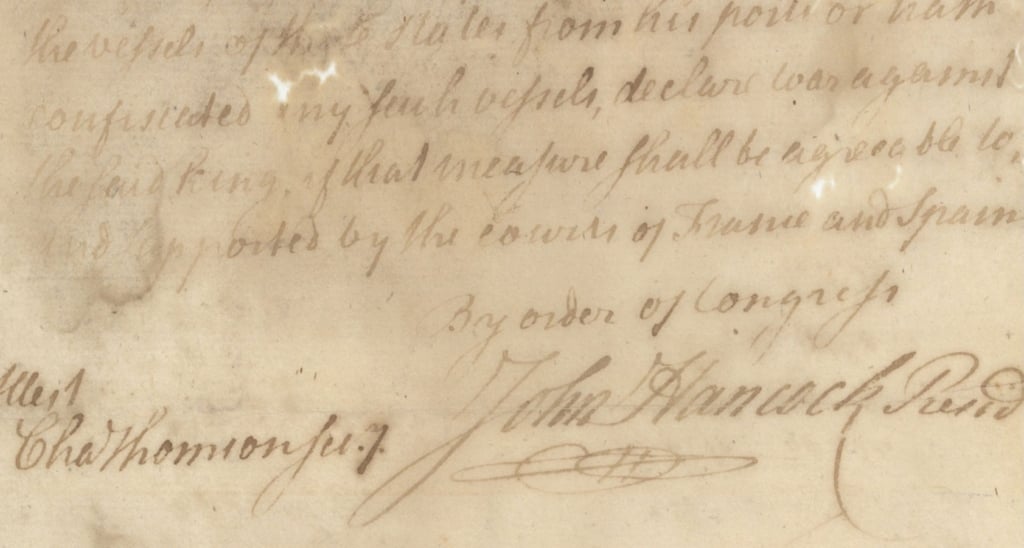

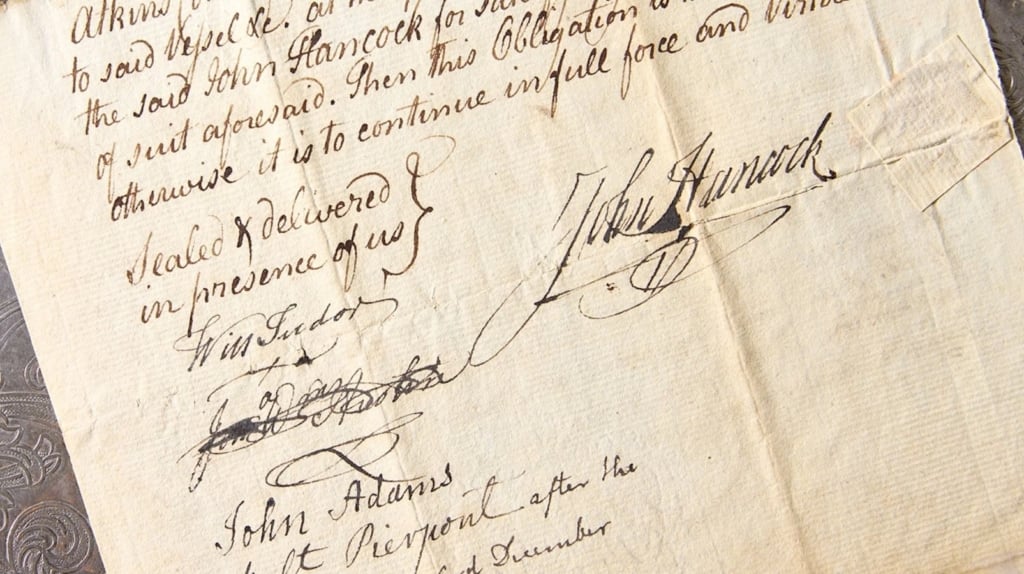

To generate meaningful statistics we needed direct comparisons, so we would require comparable quality examples of autographs of the same people over all the years and at each of the intervals. We determined to use American presidents (Washington through Clinton), and other major figures in American history such as John Hancock. Some important scientific and literary figures were also included. Each was assigned to a value group for the purposes of the study.

Below you will find the Executive Summary of the report, and will see its positive conclusions concerning the return on investment of autographs. It was illuminating to see the results and conclusions, which are good news for those who love history, yet want their acquisitions to have some type of investment aspect. But amidst these statistics, it is important to keep in mind that not every autograph will prove a good investment, so it might not be right for those uninterested in the history or who want a quick profit on their investments.

Limitations on the report: It applies solely to significant figures in the fields of history, science and literature, and not to those in entertainment, sports, or music. No statistics for these latter three fields, nor for any lesser figures in any field, were provided or analyzed. Moreover, the report was designed to provide data for the long run, to provide clarity in the form of an objective, sweeping history of autograph prices; it does not assess the individual ups and downs of the market along the way.

Dr. Wyner’s report remains the only such report of its kind.

Report on the Value of Autographed Historical Documents prepared for The Raab Collection

By Professor Abraham Wyner, Professor of Statistics, Wharton School of Business, University of Pennsylvania Executive Summary

“Background: This report analyzes a collection of 1446 historical documents with signatures from 60 great American personalities. For each document in the collection we were given the date of sale, the purchase price, and the quality of the document (with respect to a measure of historical significance). In addition, our research team accumulated much additional information including the fame of the personality, the dates of death and birth in relation to the time of sale, as well as whether or not the personality was in office (if he was a president) at the time of sale.

Results

Using a generalized method of least squares regression we were able to show that:

- Signed historical documents are investment grade opportunities.

- Since WWII the highest quality documents have averaged an annualized return of more than 10% per year.

- Even a simple autograph has demonstrated impressive growth over the last 50 years: more than 9% per year.

- Historical documents have performed comparably with the value weighted stock market.

- High quality documents performed particularly well in the last decade- outperforming the major stock market indices.

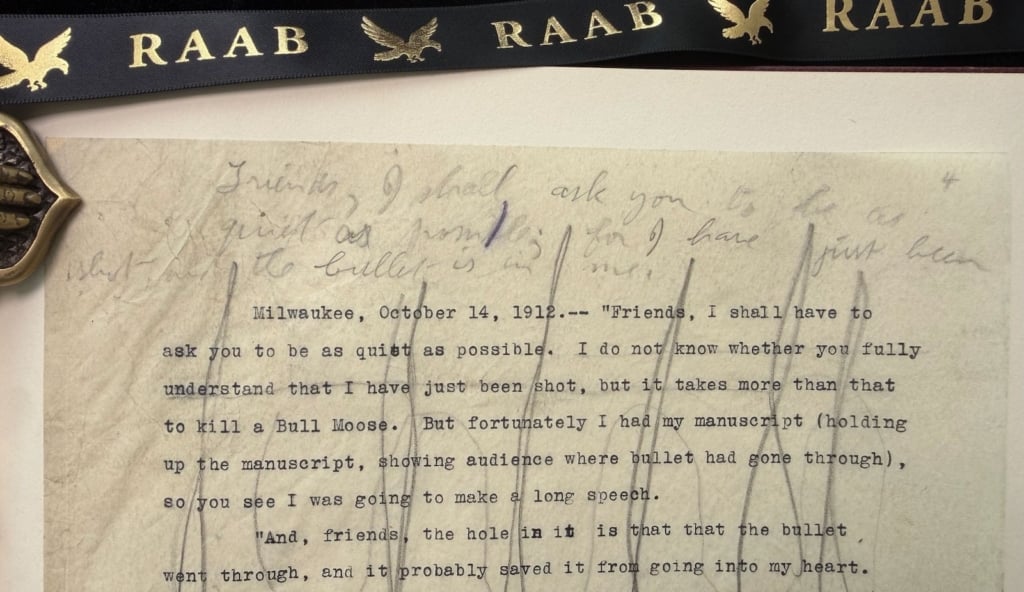

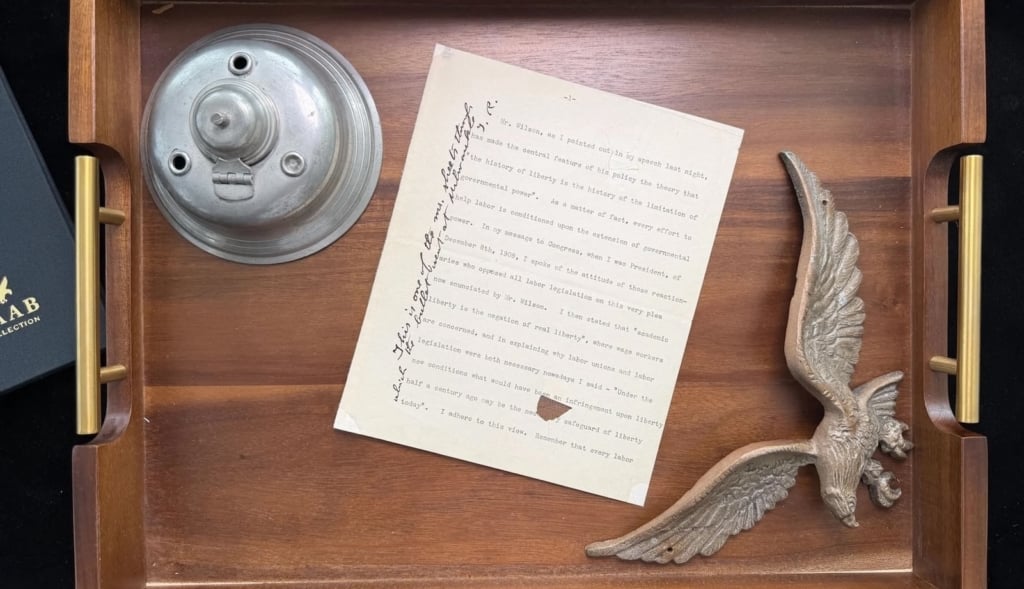

- Documents signed by Abraham Lincoln and George Washington are most expensive. When controlling and adjusting statistically for historical significance, the autographs of these two giants are almost 100 times more valuable than documents that bear the signatures of our least significant presidents: George H.W. Bush, Jimmy Carter and Gerald Ford.

Brief Technical Summary

Least squares regression is a method for determining how a combination of various different factors determines the value of a response. In this study, the response is the price of a document. The least squares technique finds the best combination of weights to predict the price. Since there are many specific factors that determine the price of a document (including chance), our model is not perfect. Using only our variables (which include no specific information about any document) we were able to explain almost 97% of the variation in the relative prices of the document.”

Coming up to date

This report was issued over a decade ago. To what extent is it still valid? Of course, the study covered a period of 110 years, so the fluctuation of the past decade would simply be one additional fluctuation among many over that time span. Looking back from the future, there might be no differential. But in terms of the market changes from 2003 until now, looking simply at those, some facts are clear. Although demand for the high-quality documents was strong in the study, that demand has substantially increased. As a result, letters and documents filling this bill have become much more difficult to find; there is in fact a scarcity. Routine letters and documents, even from significant figures, have tended to stall in this cycle, as demand has decreased. Autographs of the most notable historical figures are being sought by additional collectors, many new to the market, while those of the lesser personalities have fewer collectors following them. Some other risks known in 2003 have become more pronounced: the blizzard of questionable material in the fields of entertainment and sports has made collecting them increasingly chancy; and the unreliability of letters and certificates of authenticity issued by some so-called authenticators will leave some investors sorry to have relied on them.